The landscape of environmental reporting is transforming rapidly. As ecologists conduct field surveys across the United Kingdom in 2026, they face a new reality: their biodiversity assessments must now align with emerging global corporate disclosure standards. With the International Sustainability Standards Board (ISSB) launching its nature-related exposure draft at the UN's Convention on Biological Diversity COP17 meeting in October 2026, the intersection of ecological fieldwork and financial reporting has never been more critical. ISSB Nature-Related Disclosures in 2026: Practical Survey Protocols for Ecologists and Biodiversity Net Gain Compliance represents a fundamental shift in how biodiversity data supports both planning decisions and corporate accountability.

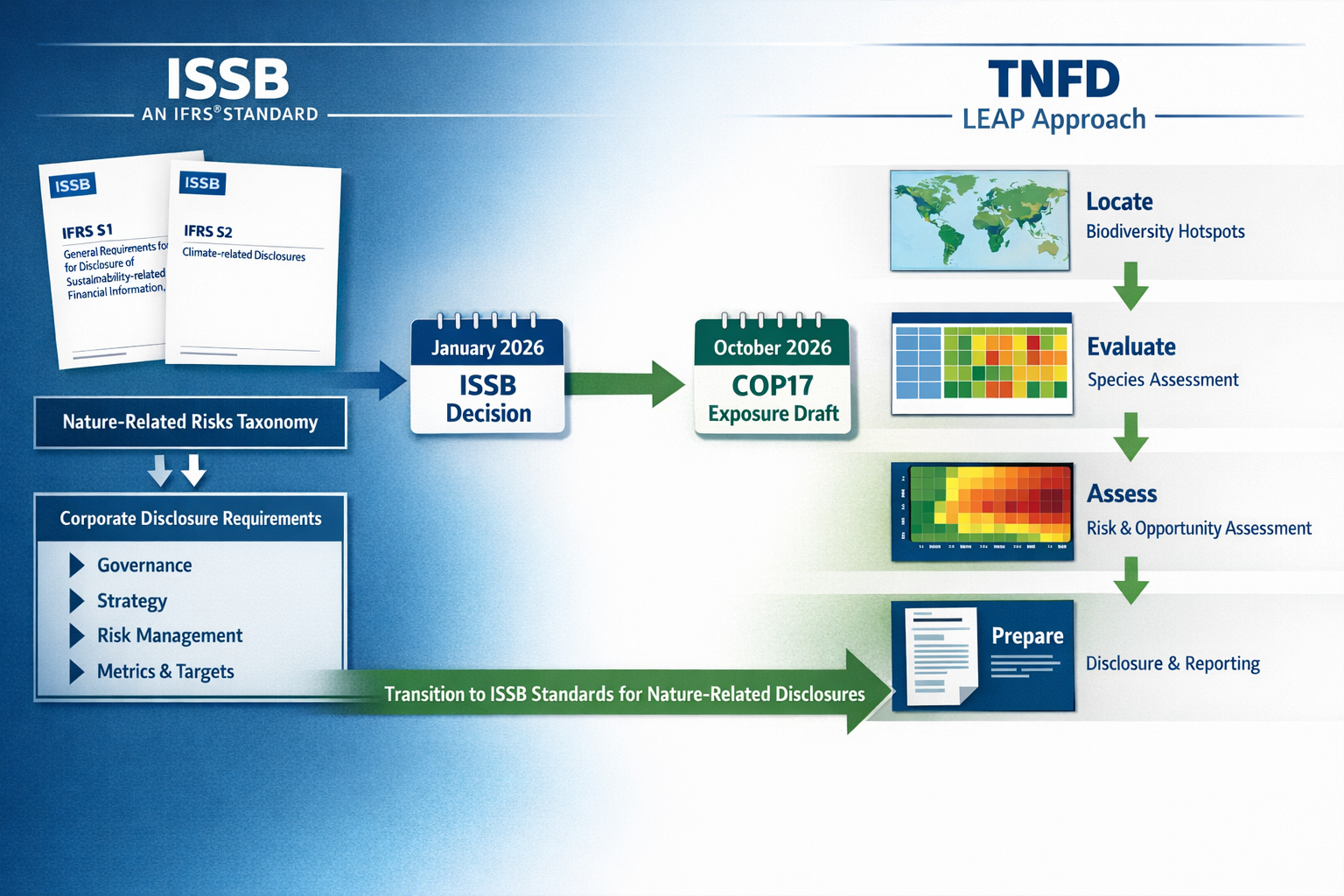

The stakes are substantial. In January 2026, all 12 ISSB members voted unanimously to proceed with standard-setting on nature-related risks and opportunities[4], building upon the Taskforce on Nature-related Financial Disclosures (TNFD) framework that over 730 companies already use[1]. For ecologists working on Biodiversity Net Gain projects, this means survey protocols must capture data that satisfies both UK planning requirements and international sustainability reporting standards.

Key Takeaways

🌿 ISSB nature standards build on TNFD: The October 2026 exposure draft will leverage the established TNFD LEAP approach (locate, evaluate, assess, and prepare), creating continuity for the 730+ companies already reporting under TNFD guidelines[1].

📊 Broad scope covers all nature-related risks: Rather than limiting focus to specific industries, the ISSB will address all nature-related risks and opportunities, including land use, pollution, water, resource extraction, and biodiversity[2][3].

✅ Existing IFRS S1 already requires material nature disclosure: Companies reporting under IFRS S1 must address material nature-related information after their first reporting year, making robust ecological survey data essential for corporate compliance[3].

🔬 Survey protocols must capture materiality metrics: Ecologists need to document not just species presence but also dependencies, impacts, risks, and opportunities that corporations must disclose under emerging standards.

⏰ Timeline demands immediate adaptation: With the exposure draft scheduled for October 2026 and TNFD completing technical work by Q3 2026, survey methodologies must evolve now to support forthcoming disclosure requirements[1].

Understanding ISSB Nature-Related Disclosures in 2026: Framework and Timeline

The ISSB Decision and Its Implications

The January 2026 ISSB meeting marked a watershed moment for nature-related financial disclosures. The Board's unanimous decision to proceed with standard-setting signals that nature-related reporting will follow the same trajectory as climate disclosures under IFRS S2[4]. This convergence creates both challenges and opportunities for ecological professionals conducting biodiversity surveys.

The ISSB's approach differs from previous voluntary frameworks in several critical ways:

Mandatory application: Unlike voluntary TNFD adoption, ISSB standards will become required disclosures for companies in jurisdictions adopting IFRS sustainability standards[3].

Comprehensive scope: The standards will encompass all nature-related risks and opportunities rather than focusing on specific sectors or environmental issues[2]. This breadth means ecological surveys must capture a wider range of data points.

Integration with existing standards: Nature disclosures will supplement IFRS S1 (General Requirements for Disclosure of Sustainability-related Financial Information) and IFRS S2 (Climate-related Disclosures)[2][3], creating an interconnected sustainability reporting framework.

Materiality-driven: Companies must identify and report material nature-related information, making the quality and comprehensiveness of baseline ecological data crucial for corporate decision-making[3].

Key Timeline Milestones

Understanding the rollout timeline helps ecologists prepare appropriate survey protocols:

| Date | Milestone | Implications for Ecologists |

|---|---|---|

| November 2025 | ISSB announces nature as next major project[1] | Begin reviewing TNFD framework alignment |

| January 2026 | Unanimous ISSB decision to proceed[4] | Confirm survey protocols capture TNFD-aligned metrics |

| Q3 2026 | TNFD completes technical work and sector guidance[1] | Incorporate final TNFD methodologies into field protocols |

| October 2026 | Exposure draft released at COP17[1][3][5] | Review draft requirements and prepare consultation responses |

| Post-October 2026 | Public consultation period[3] | Refine survey approaches based on exposure draft details |

| TBD 2027-2028 | Final standard publication | Implement fully compliant survey protocols |

Building on the TNFD Framework

The ISSB's decision to build upon TNFD's established methodology provides crucial continuity[1][6]. The LEAP approach—locate, evaluate, assess, and prepare—offers a structured framework that ecologists can integrate into survey design:

Locate: Identify where the organization or development project interfaces with nature. For Biodiversity Net Gain assessments, this involves mapping habitat boundaries, identifying priority areas, and understanding spatial relationships with protected sites.

Evaluate: Determine dependencies and impacts on nature. Survey protocols must document how development relies on ecosystem services and how activities affect biodiversity.

Assess: Identify material risks and opportunities. Ecological data should support risk assessments related to regulatory changes, physical environmental changes, and reputational factors.

Prepare: Develop disclosure-ready information. Survey outputs must be formatted to support corporate reporting requirements, not just planning applications.

Practical Survey Protocols for ISSB Nature-Related Disclosures in 2026: Field Methodology

Baseline Biodiversity Assessment Aligned with ISSB Requirements

Traditional ecological surveys focus primarily on species presence, habitat types, and protected species. However, ISSB Nature-Related Disclosures in 2026: Practical Survey Protocols for Ecologists and Biodiversity Net Gain Compliance require expanded data collection that addresses corporate materiality considerations.

Essential Data Points for ISSB Alignment

Habitat Classification and Condition

Survey protocols must document habitats using standardized classification systems that support both Biodiversity Net Gain calculations and ISSB disclosure requirements:

- Habitat type: Use UK Habitat Classification or equivalent standardized taxonomy

- Distinctiveness: Record habitat distinctiveness scores (very high, high, medium, low) per Defra Biodiversity Metric 4.0

- Condition assessment: Document condition using repeatable criteria that can be monitored over time

- Spatial extent: Measure precise area in hectares with GIS-verified boundaries

- Connectivity: Assess habitat connectivity to ecological networks and protected sites

- Strategic significance: Identify whether habitats fall within Nature Recovery Network areas or other strategic locations

Species and Ecosystem Dependencies

ISSB standards require companies to disclose dependencies on nature[1][3]. Ecological surveys should therefore document:

- Pollinator populations: Quantify pollinator diversity and abundance for developments affecting agricultural or horticultural operations

- Water regulation services: Assess wetland and riparian habitats that provide flood mitigation or water quality services

- Soil health indicators: Document soil organisms and characteristics relevant to agricultural dependencies

- Natural pest control: Identify predator-prey relationships that provide ecosystem services

- Genetic resources: Record species that may have current or future commercial value

Impact Pathways and Materiality Triggers

Survey data should enable impact pathway analysis:

- Direct habitat loss: Quantify habitat area affected by development footprint

- Fragmentation effects: Model connectivity changes and barrier effects

- Hydrological changes: Assess impacts on water-dependent habitats and species

- Pollution pathways: Identify sensitive receptors for air, water, or soil contamination

- Invasive species vectors: Document existing invasive species and introduction risks

- Climate vulnerability: Assess habitat and species sensitivity to climate change

TNFD LEAP Integration in Field Protocols

Locate Phase: Spatial Analysis Requirements

The TNFD Locate phase requires understanding where operations interface with nature[1]. For development projects, this translates to specific survey requirements:

Priority Area Screening

Before conducting detailed surveys, ecologists should screen the site against:

- Protected sites: Distance to and potential impacts on SACs, SPAs, SSSIs, Ramsar sites, National Parks, and AONBs

- Ancient woodland: Presence of or proximity to irreplaceable habitats

- Priority habitats: Presence of Section 41 habitats of principal importance

- Biodiversity opportunity areas: Location within Local Nature Recovery Strategy priority areas

- Water catchments: Position within sensitive water catchments or groundwater source protection zones

- Species records: Desktop review of protected and priority species within 2km

Spatial Data Collection Standards

Field surveys must generate GIS-compatible spatial data:

- GPS accuracy: Minimum 5-meter accuracy for habitat boundaries; sub-meter accuracy for specific features

- Coordinate system: British National Grid (EPSG:27700) for UK projects

- Metadata: Complete attribute tables including survey date, surveyor, weather conditions, and confidence levels

- Photo documentation: Geotagged photographs with cardinal direction and scale references

- Boundary verification: Ground-truthed boundaries cross-referenced with aerial imagery

Evaluate Phase: Dependencies and Impacts Assessment

The Evaluate phase requires systematic assessment of nature dependencies and impacts[1]. Survey protocols should include:

Ecosystem Service Assessment

Document ecosystem services relevant to the development and surrounding land uses:

- Provisioning services: Timber, food, freshwater, genetic resources

- Regulating services: Climate regulation, flood control, water purification, pollination

- Cultural services: Recreation, aesthetic value, cultural heritage

- Supporting services: Soil formation, nutrient cycling, primary production

Impact Magnitude Scoring

For each identified impact, record:

- Spatial extent: Area affected (site-level, local, regional, national, international)

- Duration: Temporary (< 1 year), short-term (1-7 years), medium-term (7-25 years), long-term (> 25 years), permanent

- Reversibility: Reversible, reversible with intervention, irreversible

- Frequency: One-time, intermittent, continuous

- Magnitude: Negligible, minor, moderate, major, severe

Assess Phase: Risk and Opportunity Identification

The Assess phase connects ecological data to business risks and opportunities[1]. Survey outputs should support:

Regulatory Risk Assessment

- BNG compliance risk: Calculate baseline biodiversity units and identify constraints to achieving 10% net gain

- Protected species licensing: Identify species requiring licenses and associated timeline/cost implications

- Nutrient neutrality: Assess nutrient budget implications for developments in sensitive catchments

- Future policy exposure: Identify features that may face stricter protection under emerging policies

Physical Risk Documentation

- Climate vulnerability: Assess habitat and species sensitivity to projected climate changes

- Ecosystem degradation: Document existing condition trends that may affect long-term viability

- Invasive species risk: Identify pathways for invasive species that could degrade habitats

- Pollution sensitivity: Record sensitivity to air, water, or soil quality changes

Opportunity Identification

- Enhancement potential: Identify degraded habitats with high restoration potential

- Biodiversity credit generation: Assess suitability for creating and selling biodiversity units

- Ecosystem service enhancement: Identify opportunities to increase natural capital value

- Biodiversity offsetting: Evaluate potential for off-site biodiversity delivery

Prepare Phase: Disclosure-Ready Data Collection

The Prepare phase focuses on generating information suitable for corporate disclosure[1]. Ecological surveys should produce:

Quantitative Metrics

- Biodiversity units: Calculate baseline and post-development biodiversity units using Defra Metric 4.0

- Habitat area: Precise measurements in hectares by habitat type and condition

- Species abundance: Quantified population estimates for key species groups

- Ecosystem service values: Where feasible, quantified ecosystem service provision

- Trend data: Year-on-year changes in biodiversity metrics for monitoring purposes

Qualitative Assessments

- Materiality narrative: Written assessment of why nature-related factors are material to the project

- Dependency description: Clear explanation of how the project or organization depends on nature

- Impact pathways: Narrative description of cause-effect relationships

- Management measures: Documentation of mitigation hierarchy application and enhancement strategies

Biodiversity Net Gain Compliance Integration

The UK's mandatory Biodiversity Net Gain requirement creates a natural alignment point between planning requirements and ISSB disclosure needs. Survey protocols that satisfy BNG assessment requirements can be expanded to support ISSB disclosures.

Enhanced BNG Survey Protocols

Baseline Habitat Survey

Standard BNG surveys should be enhanced with ISSB-relevant data:

- Extended survey area: Survey beyond the development boundary to capture landscape-scale dependencies and impacts

- Ecosystem service mapping: Document ecosystem services provided by baseline habitats

- Climate resilience assessment: Evaluate habitat vulnerability to climate change

- Stakeholder value: Record cultural and recreational values associated with habitats

- Supply chain connections: Identify how habitats support supply chain dependencies (e.g., pollination for agriculture)

Temporal Considerations

ISSB disclosures require forward-looking information[3]. Surveys should therefore include:

- Seasonal variation: Multi-season surveys to capture temporal biodiversity patterns

- Monitoring protocols: Establish repeatable methodologies for long-term monitoring

- Trend analysis: Where possible, compare current conditions to historical data

- Projection modeling: Use survey data to model future biodiversity trajectories under different management scenarios

Metric 4.0 Enhancements

The Defra Biodiversity Metric 4.0 provides the calculation framework for BNG, but ISSB alignment requires additional documentation:

- Uncertainty quantification: Document confidence levels in habitat classification and condition assessments

- Alternative scenarios: Model biodiversity outcomes under different development and management options

- Additionality demonstration: Clearly document how enhancement measures exceed legal requirements

- Long-term security: Provide evidence of 30-year habitat management and monitoring commitments

Survey Checklists and Quality Assurance for ISSB Nature-Related Disclosures in 2026

Pre-Survey Planning Checklist

Effective ISSB Nature-Related Disclosures in 2026: Practical Survey Protocols for Ecologists and Biodiversity Net Gain Compliance begin with thorough planning:

Scope Definition

✅ Define survey area including development site and appropriate buffer zones

✅ Identify all relevant regulatory requirements (BNG, protected species, ISSB disclosure needs)

✅ Determine materiality thresholds for nature-related risks and opportunities

✅ Establish client reporting requirements and disclosure timelines

✅ Review corporate sustainability commitments and targets

Desktop Study

✅ Obtain and review aerial imagery (current and historical)

✅ Access Multi-Agency Geographic Information for the Countryside (MAGIC) data

✅ Review local biological records center data

✅ Obtain Phase 1 habitat survey data if available

✅ Review planning history and environmental statements

✅ Identify designated sites within 10km

✅ Review Local Nature Recovery Strategy and biodiversity opportunity areas

✅ Assess climate projections for the region

Survey Design

✅ Select appropriate survey methodologies for habitats and species present

✅ Determine optimal survey timing based on target species and habitats

✅ Prepare survey forms aligned with TNFD LEAP framework

✅ Configure GPS/GIS equipment with appropriate coordinate systems

✅ Prepare photographic equipment with geotagging capability

✅ Arrange access permissions and landowner notifications

✅ Conduct health and safety risk assessment

Field Survey Execution Checklist

Habitat Assessment

✅ Record habitat types using UK Habitat Classification

✅ Assess habitat condition using Defra Metric 4.0 condition sheets

✅ Measure precise habitat areas using GPS/GIS

✅ Document habitat connectivity and ecological networks

✅ Photograph representative areas with scale and direction references

✅ Record evidence of ecosystem services provision

✅ Note signs of degradation, invasive species, or pollution

✅ Assess climate vulnerability indicators

Species Surveys

✅ Conduct species surveys appropriate to season and habitat

✅ Record protected and priority species with precise locations

✅ Quantify abundance using appropriate methodologies

✅ Document species dependencies on habitats

✅ Identify species of commercial or cultural significance

✅ Note invasive non-native species

✅ Collect voucher specimens or photographs where appropriate

ISSB-Specific Data Collection

✅ Document nature dependencies relevant to development or corporate operations

✅ Identify impact pathways and affected receptors

✅ Record potential regulatory risks (licensing, nutrient neutrality, etc.)

✅ Note enhancement and offsetting opportunities

✅ Assess alignment with corporate sustainability targets

✅ Document stakeholder interests in natural features

✅ Record climate resilience factors

Post-Survey Quality Assurance

Data Validation

✅ Verify GPS coordinates and spatial data accuracy

✅ Cross-reference habitat classifications with aerial imagery

✅ Validate species identifications with reference materials or specialists

✅ Check calculation accuracy for biodiversity units

✅ Ensure photographic documentation is complete and geotagged

✅ Verify all survey forms are complete with no data gaps

ISSB Alignment Review

✅ Confirm survey data addresses all four LEAP phases

✅ Verify materiality assessment is supported by quantitative data

✅ Ensure dependencies and impacts are clearly documented

✅ Check that risks and opportunities are identified and characterized

✅ Confirm data is formatted for disclosure purposes

✅ Verify temporal considerations are addressed

Reporting Standards

✅ Prepare survey report following BNG assessment structure

✅ Include ISSB-specific sections on dependencies, impacts, risks, and opportunities

✅ Provide clear quantitative metrics (biodiversity units, habitat areas, species populations)

✅ Include GIS maps showing spatial relationships

✅ Document uncertainty and confidence levels

✅ Provide recommendations aligned with mitigation hierarchy

✅ Include monitoring and adaptive management protocols

Common Pitfalls and How to Avoid Them

Insufficient Spatial Scope

❌ Pitfall: Surveying only the development footprint without considering landscape-scale dependencies

✅ Solution: Extend survey area to capture ecosystem service provision areas, connectivity corridors, and downstream receptors

Inadequate Temporal Coverage

❌ Pitfall: Single-season surveys that miss key species or habitat conditions

✅ Solution: Conduct multi-season surveys aligned with species activity patterns and habitat phenology

Missing Materiality Context

❌ Pitfall: Collecting ecological data without understanding corporate materiality thresholds

✅ Solution: Engage with corporate sustainability teams early to understand disclosure requirements and materiality criteria

Poor Documentation of Uncertainty

❌ Pitfall: Presenting survey results without confidence levels or uncertainty ranges

✅ Solution: Systematically document survey limitations, confidence levels, and data gaps

Failure to Future-Proof Data

❌ Pitfall: Collecting data that satisfies current requirements but cannot support future monitoring

✅ Solution: Establish repeatable methodologies and baseline datasets that enable long-term trend analysis

Integrating Ecological Data with Corporate ISSB Disclosures

From Field Data to Financial Materiality

The bridge between ecological survey data and corporate disclosure requires translating environmental information into business-relevant metrics. This translation process involves several key steps:

Dependency Mapping

Ecological surveys must identify and quantify how business operations depend on nature. For development projects, this includes:

- Water dependency: Quantify water requirements and assess availability from natural sources

- Pollination services: For agricultural or horticultural developments, assess pollinator populations and habitat

- Climate regulation: Document vegetation that provides cooling, shade, or microclimate regulation

- Flood mitigation: Assess natural flood storage and water regulation services

- Soil stability: Evaluate vegetation's role in preventing erosion or land instability

Impact Quantification

Survey data should support quantified impact assessments:

- Habitat loss: Precise area calculations by habitat type and distinctiveness

- Species population effects: Estimated population-level impacts on key species

- Ecosystem service reduction: Quantified changes in service provision (e.g., carbon storage, flood retention)

- Connectivity disruption: Modeled effects on species movement and gene flow

- Cumulative effects: Assessment of combined impacts with other developments

Risk Translation

Ecological risks must be expressed in business terms:

- Regulatory risk: Probability and cost of licensing delays, planning refusals, or enforcement action

- Reputational risk: Potential for public opposition, NGO campaigns, or brand damage

- Operational risk: Likelihood of construction delays due to protected species or habitat constraints

- Financial risk: Cost implications of mitigation measures, offsetting requirements, or statutory biodiversity credits

- Transition risk: Exposure to changing environmental regulations and standards

Materiality Assessment Framework

The ISSB requires companies to assess whether nature-related information is material to investors[3]. Ecologists can support this assessment by providing:

Quantitative Materiality Indicators

- Financial magnitude: Cost of BNG compliance, offsetting, or mitigation measures relative to project value

- Regulatory exposure: Probability of regulatory intervention based on protected species or habitat presence

- Timeline impact: Potential delay to project delivery due to ecological constraints

- Market sensitivity: Stakeholder interest levels in biodiversity features

- Precedent analysis: Comparison with similar projects that faced nature-related challenges

Qualitative Materiality Factors

- Irreplaceability: Presence of ancient woodland, irreplaceable habitats, or unique species assemblages

- Strategic significance: Location within Nature Recovery Network or other priority areas

- Stakeholder salience: Level of public, NGO, or regulatory interest

- Reputational sensitivity: Potential for nature-related issues to affect corporate reputation

- Cumulative context: Contribution to wider environmental pressures or trends

Supporting IFRS S1 and S2 Integration

ISSB nature disclosures will supplement existing IFRS S1 (general sustainability) and S2 (climate) standards[2][3]. Ecological surveys should therefore capture data that supports integrated reporting:

Climate-Nature Linkages

- Carbon storage: Quantify carbon sequestration and storage in habitats

- Climate adaptation: Assess how habitats contribute to climate resilience

- Nature-based solutions: Identify opportunities for habitats to support climate mitigation

- Climate vulnerability: Evaluate how climate change affects biodiversity features

- Co-benefits: Document where nature conservation delivers climate benefits

Governance and Strategy Alignment

Survey reports should include sections that support corporate governance disclosures:

- Policy alignment: Assessment of project alignment with corporate biodiversity commitments

- Target contribution: Quantification of project contribution to corporate nature-positive targets

- Risk management: Integration with corporate environmental risk management frameworks

- Scenario analysis: Data supporting nature-related scenario modeling

Case Study Applications: ISSB Nature-Related Disclosures in Practice

Residential Development with Ancient Woodland Buffer

Project Context: A 150-unit residential development adjacent to ancient woodland, undertaken by a publicly traded property developer committed to ISSB disclosure.

Survey Approach:

The ecological team extended surveys 200 meters beyond the development boundary to capture:

- Ancient woodland condition and buffer zone impacts

- Bat populations using woodland for roosting and foraging

- Great crested newt populations in ponds within 500m

- Hedgerow connectivity between woodland and wider landscape

- Soil carbon stocks in existing grassland

ISSB-Aligned Outputs:

Dependencies Identified:

- Development relied on sustainable drainage systems dependent on soil infiltration capacity

- Landscape design required locally sourced native plants, dependent on regional nursery supply chains

- Resident amenity value dependent on proximity to ancient woodland

Material Risks Documented:

- High regulatory risk: Great crested newt licensing could delay construction by 6-12 months (estimated cost: £250,000-500,000)

- Reputational risk: Ancient woodland buffer zone controversy could affect brand reputation and future planning applications

- Physical risk: Climate change projecting increased drought stress on ancient woodland, potentially affecting amenity value

Opportunities Captured:

- 15% biodiversity net gain achievable through woodland buffer enhancement and hedgerow restoration

- Potential to generate biodiversity credits for sale from off-site habitat creation

- Marketing advantage from nature-positive positioning

Corporate Disclosure Support:

The survey data enabled the developer to disclose:

- £750,000 investment in nature-related mitigation and enhancement

- Contribution to corporate 2030 nature-positive target

- Integration of nature considerations into project governance from inception

- Monitoring protocol supporting 30-year accountability

Agricultural Land Conversion with Pollinator Dependencies

Project Context: Conversion of agricultural land to industrial use, with corporate client dependent on agricultural supply chains.

Survey Approach:

Extended surveys captured:

- Baseline pollinator diversity and abundance

- Flowering plant resources across seasons

- Connectivity to nearby agricultural land

- Soil health indicators

- Water quality in adjacent watercourse

ISSB-Aligned Outputs:

Dependencies Identified:

- Corporate supply chain dependent on pollination services for fruit and vegetable suppliers within 50km

- Regional agricultural productivity dependent on pollinator populations

- Water quality dependent on riparian vegetation and soil management

Material Risks Documented:

- Transition risk: Increasing pollinator protection regulations could restrict future development options

- Supply chain risk: Pollinator decline could affect agricultural supplier viability

- Regulatory risk: Nutrient neutrality requirements added £180,000 to project costs

Opportunities Captured:

- Creation of 2.5 hectares of wildflower habitat supporting pollinators

- Partnership with local farmers to enhance field margins

- Corporate leadership positioning on nature-positive agriculture

This case demonstrates how benefitting nature and developers can align through comprehensive survey protocols.

Infrastructure Project with Water Dependency

Project Context: Major infrastructure development affecting wetland habitats, undertaken by utility company with ISSB reporting obligations.

Survey Approach:

Comprehensive wetland assessment including:

- National Vegetation Classification (NVC) survey

- Water vole and otter surveys

- Invertebrate sampling

- Hydrological assessment

- Water quality monitoring

- Ecosystem service valuation

ISSB-Aligned Outputs:

Dependencies Identified:

- Infrastructure operation dependent on water abstraction regulated by wetland environmental flows

- Flood protection dependent on wetland water storage capacity

- Operational resilience dependent on climate-regulated water availability

Material Risks Documented:

- Physical risk: Wetland degradation could reduce flood storage, increasing infrastructure flood risk (estimated asset exposure: £15 million)

- Regulatory risk: Water abstraction license restrictions could affect operational capacity

- Climate risk: Projected changes in precipitation patterns could affect wetland hydrology and dependent species

Opportunities Captured:

- Wetland creation delivering 25% biodiversity net gain

- Natural flood management reducing downstream infrastructure costs

- Carbon sequestration in created wetlands contributing to net-zero targets

Corporate Disclosure Support:

Survey data enabled disclosure of:

- £2.3 million investment in nature-based solutions

- Quantified climate adaptation benefits from wetland creation

- Integration of nature considerations into asset management strategy

- Long-term monitoring supporting adaptive management

Future-Proofing Survey Protocols for Evolving Standards

Preparing for the October 2026 Exposure Draft

With the ISSB exposure draft scheduled for release at COP17 in October 2026[1][3][5], ecologists should prepare for potential refinement of survey requirements:

Anticipated Disclosure Elements

Based on TNFD precedent and ISSB climate standards, the nature exposure draft will likely require:

- Governance disclosures: How nature-related risks are overseen at board and management levels

- Strategy disclosures: How nature dependencies, impacts, risks, and opportunities affect strategy

- Risk management disclosures: Processes for identifying, assessing, and managing nature-related risks

- Metrics and targets: Quantitative measures of nature-related performance and progress toward targets

Survey Protocol Adaptations

To prepare for these disclosure categories, survey protocols should:

- Establish baseline metrics: Create repeatable quantitative measures that can track progress over time

- Document governance integration: Record how survey findings inform project decision-making

- Support scenario analysis: Provide data enabling modeling of different management scenarios

- Enable target-setting: Quantify enhancement potential to support nature-positive target development

Monitoring and Adaptive Management Frameworks

ISSB disclosures will require ongoing reporting, not just one-time assessments[3]. Survey protocols must therefore establish long-term monitoring frameworks:

Monitoring Protocol Design

- Repeatable methodologies: Use standardized approaches that different surveyors can replicate

- Appropriate frequency: Align monitoring intervals with ecological change rates and reporting cycles

- Trigger thresholds: Define conditions that would require management intervention

- Data management: Establish systems for long-term data storage and accessibility

- Quality assurance: Build in verification and validation procedures

Adaptive Management Integration

- Clear objectives: Define measurable targets for biodiversity outcomes

- Monitoring indicators: Select indicators that reliably reflect progress toward objectives

- Decision rules: Establish criteria for when management changes are needed

- Intervention options: Pre-identify potential management responses to different scenarios

- Learning loops: Create processes for incorporating monitoring results into strategy updates

Technology Integration and Innovation

Emerging technologies offer opportunities to enhance survey efficiency and data quality:

Remote Sensing and AI

- Habitat mapping: Use satellite or drone imagery with AI classification to map habitats cost-effectively

- Change detection: Automated detection of habitat changes over time

- Species identification: AI-powered acoustic monitoring for birds and bats; camera traps with automated species recognition

- Condition assessment: Remote sensing indicators of habitat condition (vegetation indices, structure metrics)

Digital Data Management

- Field data apps: Mobile applications enabling real-time data entry with validation rules

- Cloud-based databases: Centralized data storage supporting multi-site, multi-year analysis

- GIS integration: Seamless integration of field data with spatial analysis tools

- Blockchain verification: Emerging use of blockchain for verifiable biodiversity credit tracking

Collaborative Platforms

- Data sharing: Platforms enabling ecologists, developers, and corporations to access shared data

- Stakeholder engagement: Digital tools for communicating survey findings to diverse audiences

- Transparency: Public-facing dashboards showing biodiversity monitoring results

Conclusion: Implementing ISSB Nature-Related Disclosures in 2026

The convergence of Biodiversity Net Gain requirements and emerging ISSB nature-related disclosure standards creates both challenges and opportunities for ecological professionals. ISSB Nature-Related Disclosures in 2026: Practical Survey Protocols for Ecologists and Biodiversity Net Gain Compliance requires a fundamental shift in how surveys are designed, executed, and reported.

The January 2026 unanimous ISSB decision[4] signals that nature-related financial disclosure will become as standardized and mandatory as climate reporting. For ecologists, this means survey protocols must evolve beyond traditional species and habitat assessment to capture the dependencies, impacts, risks, and opportunities that corporations must disclose to investors.

The TNFD LEAP framework provides a proven methodology that ecologists can integrate into field protocols immediately[1]. By systematically locating nature interfaces, evaluating dependencies and impacts, assessing material risks and opportunities, and preparing disclosure-ready data, ecological surveys can serve dual purposes: satisfying UK planning requirements while supporting global corporate accountability.

Actionable Next Steps

For ecologists and biodiversity professionals seeking to align with ISSB standards:

Immediate Actions (Q2-Q3 2026):

- Review TNFD framework: Familiarize yourself with TNFD recommendations and the LEAP approach to understand disclosure requirements

- Enhance survey templates: Modify field survey forms to capture ISSB-relevant data on dependencies, impacts, risks, and opportunities

- Engage corporate clients: Initiate conversations with clients about their ISSB disclosure timelines and materiality thresholds

- Upgrade spatial data: Ensure GIS capabilities support landscape-scale analysis beyond development boundaries

- Build monitoring frameworks: Design repeatable protocols that enable long-term trend analysis

Medium-Term Actions (Q4 2026-Q1 2027):

- Review exposure draft: Analyze the October 2026 ISSB exposure draft to identify specific disclosure requirements

- Participate in consultation: Submit consultation responses based on practical field experience

- Develop case studies: Document projects demonstrating ISSB-aligned survey approaches

- Invest in technology: Implement remote sensing, AI, and digital data management tools

- Build partnerships: Collaborate with corporate sustainability teams, financial advisors, and disclosure specialists

Long-Term Actions (2027 onwards):

- Implement final standards: Adapt protocols to final ISSB nature standards when published

- Continuous improvement: Refine methodologies based on monitoring results and emerging best practices

- Thought leadership: Share learnings to advance the profession's capacity for disclosure-aligned surveys

- Integrate frameworks: Ensure survey approaches support achieving biodiversity net gain without risk while meeting ISSB requirements

The path forward requires ecological professionals to expand their skill sets, embrace new technologies, and understand the business context of nature-related financial disclosure. Those who successfully navigate this transition will not only comply with emerging standards but will also position themselves as essential partners in the global shift toward nature-positive business practices.

The October 2026 exposure draft will provide crucial clarity on specific requirements, but the direction is clear: nature-related disclosure is becoming mandatory, standardized, and financially material. Ecologists who adapt their survey protocols now will be well-positioned to support both biodiversity net gain compliance and corporate sustainability accountability in the years ahead.

The integration of ecological expertise with corporate disclosure represents a historic opportunity to elevate nature's importance in business decision-making. By delivering robust, disclosure-ready biodiversity data, ecologists can ensure that nature's value is properly recognized, protected, and enhanced across the development sector and beyond.

References

[1] Issb January 2026 – https://www.spglobal.com/sustainable1/en/insights/regulatory-tracker/issb-january-2026

[2] Issb Considers Creating Nature Related Standards – https://practicalesg.com/2026/01/issb-considers-creating-nature-related-standards/

[3] Issb Nature Reporting – https://kpmg.com/xx/en/our-insights/ifrg/2026/issb-nature-reporting.html

[4] Issb Update January 2026 – https://www.ifrs.org/news-and-events/updates/issb/2026/issb-update-january-2026/

[5] Undp And Bmukn Welcome Issbs Decision Advance Nature Related Standard Setting Based Tnfd Framework – https://www.undp.org/nature/news/undp-and-bmukn-welcome-issbs-decision-advance-nature-related-standard-setting-based-tnfd-framework

[6] Issb Decision On Nature Related Standard Setting Drawing On Tnfd Framework – https://tnfd.global/issb-decision-on-nature-related-standard-setting-drawing-on-tnfd-framework/

[7] Issb Meeting Summaries – https://www.iasplus.com/en/news/2026/02/issb-meeting-summaries

[8] Issb Staff Outline Proposed Approach For Nature Standard Setting – https://www.responsible-investor.com/issb-staff-outline-proposed-approach-for-nature-standard-setting/

[9] Businesses And Governments Master The Energy Nexus – https://www.weforum.org/stories/2026/02/businesses-and-governments-master-the-energy-nexus/

[10] Sustainability Reporting In 2026 – https://www.slaughterandmay.com/horizon-scanning/2026/governance-and-sustainability/sustainability-reporting-in-2026/