As the International Sustainability Standards Board (ISSB) prepares to release its groundbreaking Exposure Draft on nature-related disclosures in October 2026, ecologists and biodiversity professionals face an unprecedented opportunity. The convergence of ISSB Nature Disclosures and BNG: Survey Protocols for Ecologists Meeting 2026 Corporate Reporting Standards represents a transformative moment where field-level ecological data will directly inform investor-grade corporate reporting. This shift demands that ecological survey methodologies evolve to capture not just habitat quality, but the financial materiality of nature dependencies and impacts.

The timing couldn't be more critical. With the ISSB's decision in January 2026 to proceed with comprehensive standard-setting covering all material nature-related risks and opportunities, ecological practitioners must now understand how their field protocols align with emerging corporate disclosure requirements. This integration of Biodiversity Net Gain (BNG) assessments with international financial reporting standards creates new expectations for data quality, consistency, and business relevance.

Key Takeaways

- 🌍 ISSB's October 2026 Exposure Draft will establish global standards for nature-related disclosures, requiring ecologists to align survey protocols with investor-grade reporting requirements

- 📊 Survey data must now quantify financial materiality of nature dependencies, moving beyond traditional habitat assessments to measure corporate risks and opportunities

- 🔄 BNG methodologies provide the foundation for meeting ISSB requirements, with biodiversity metrics translating directly into corporate disclosure frameworks

- ⏰ The 120-day consultation period following the October draft offers ecologists a critical window to shape standards that affect field protocols

- 💼 Cross-sector applicability means survey protocols must serve multiple stakeholders: planners, developers, investors, and corporate sustainability teams

Understanding the ISSB Nature Disclosure Framework for 2026

What the ISSB Decided in January 2026

The ISSB's pivotal meeting on 28 January 2026 marked a watershed moment for nature-related corporate reporting. The Board made the strategic decision to develop standards covering all material nature-related risks and opportunities affecting entity prospects, rather than limiting scope to specific sectors or biodiversity hotspots. This comprehensive approach means that ecological survey data will need to support disclosure requirements across diverse industries and geographies.

The project, previously known as "Biodiversity, Ecosystems and Ecosystem Services (BEES)," was streamlined to "Nature-related Disclosures" in February 2026. This rebranding reflects a broader scope that mirrors the successful IFRS S2 Climate-related Disclosures standard. For ecologists, this parallel structure provides a familiar framework: just as climate disclosures quantify carbon impacts and transition risks, nature disclosures will quantify biodiversity impacts and ecosystem dependencies.

Key Concepts Ecologists Must Understand

The ISSB staff has recommended formal definitions for several essential terms that will shape how ecological data feeds into corporate reporting:

- Nature-related risks: Potential negative impacts on company value arising from dependencies or impacts on nature

- Nature-related physical risks: Direct threats from ecosystem degradation (e.g., loss of pollination services, water scarcity)

- Nature-related transition risks: Business impacts from policy changes, market shifts, or stakeholder pressure related to nature protection

- Nature-related opportunities: Potential value creation through nature-positive business models or ecosystem restoration

These definitions require ecologists to think beyond traditional conservation metrics. When conducting biodiversity impact assessments, surveyors must now consider how findings translate into financial materiality for corporate stakeholders.

The October 2026 Timeline and COP17 Alignment

The strategic timing of the Exposure Draft release in October 2026 aligns with the Convention on Biological Diversity's COP17 meeting. This synchronization ensures that corporate disclosure standards develop alongside international biodiversity policy frameworks. The planned 120-day public comment period extends into early 2027, giving ecological professionals time to review technical requirements and provide feedback on survey protocol implications.

For practitioners conducting BNG assessments in 2026, this timeline means preparing for enhanced data requirements that will likely become mandatory in subsequent years. Early adopters who align their methodologies now will gain competitive advantages as corporate clients seek compliant ecological consultants.

Aligning BNG Survey Protocols with ISSB Nature Disclosures and 2026 Corporate Reporting Standards

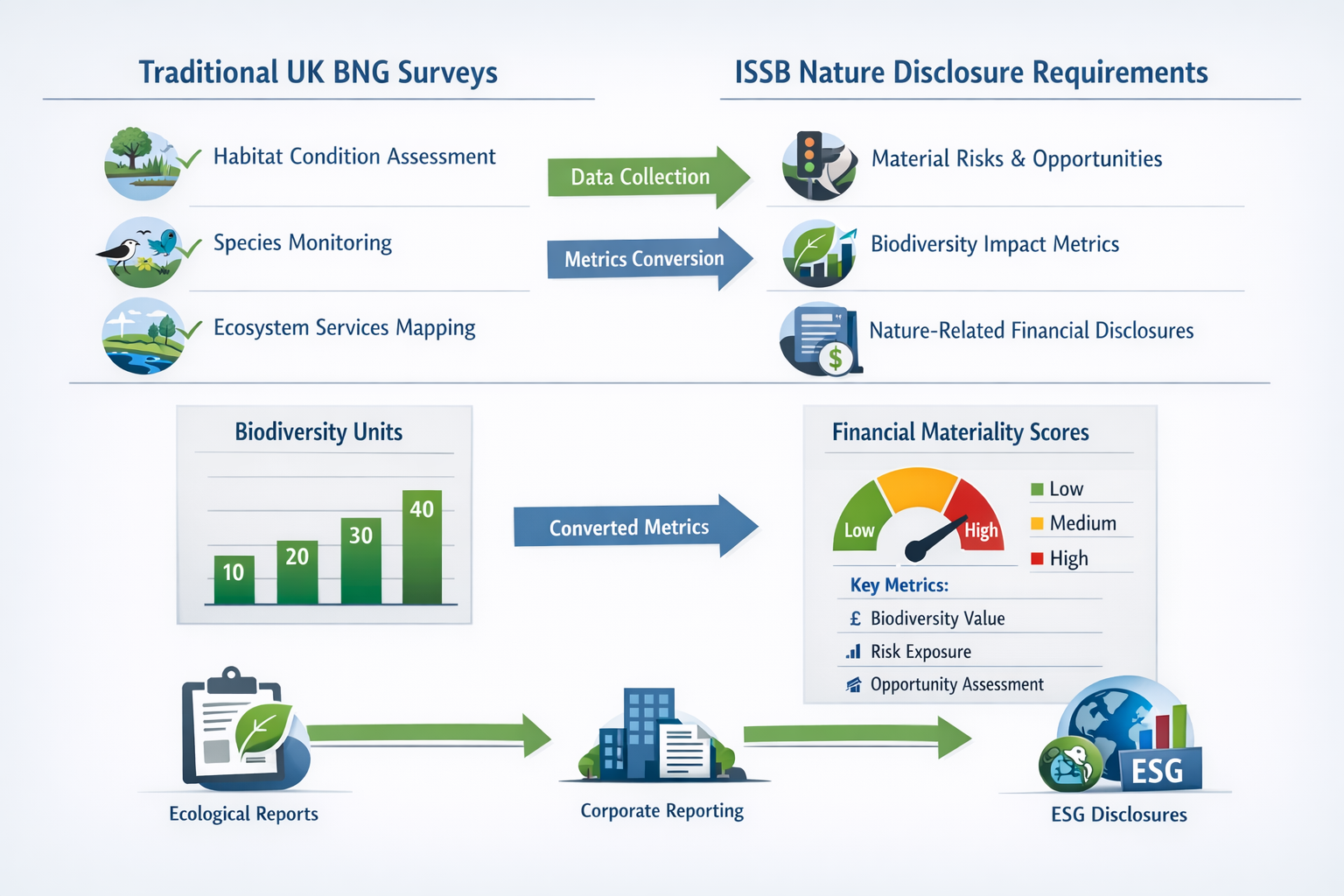

From Habitat Units to Financial Materiality

Traditional UK Biodiversity Net Gain assessments focus on calculating biodiversity units through habitat condition assessments, distinctiveness ratings, and strategic significance multipliers. While these metrics serve planning purposes effectively, ISSB nature disclosures require additional layers of analysis that connect ecological data to financial outcomes.

Ecologists must now answer questions beyond "How many biodiversity units exist?" to address "What financial risks does ecosystem degradation pose to business operations?" This evolution demands:

- Dependency mapping: Identifying which ecosystem services directly support business activities (water filtration, pollination, climate regulation)

- Impact quantification: Measuring how development or operations affect nature in ways that create regulatory, reputational, or operational risks

- Opportunity identification: Recognizing where nature-positive interventions create business value through enhanced ecosystem services or market differentiation

When planning biodiversity projects, surveyors should incorporate these financial materiality considerations into baseline assessments and monitoring protocols.

Enhanced Data Collection Requirements

Meeting ISSB Nature Disclosures and BNG: Survey Protocols for Ecologists Meeting 2026 Corporate Reporting Standards requires upgrading traditional survey methodologies:

Baseline Assessments Must Include:

- 📋 Ecosystem service dependency inventories

- 📊 Quantified risk exposure metrics (not just habitat quality scores)

- 🗺️ Spatial analysis of nature-related physical risks

- 💰 Preliminary financial impact assessments

- 📈 Trend analysis showing temporal changes in nature dependencies

Monitoring Protocols Should Capture:

- Effectiveness of nature-positive interventions

- Changes in ecosystem service provision over time

- Early warning indicators of physical risk materialization

- Compliance metrics for transition risk management

- Stakeholder engagement outcomes related to nature impacts

These enhanced requirements don't replace existing BNG methodologies but supplement them with investor-relevant context. Developers seeking to achieve 10% BNG will find that ISSB-aligned protocols provide additional value by supporting corporate sustainability reporting requirements.

Sector-Specific Considerations

While the ISSB decided against sector-limited standards, different industries will experience varying levels of nature dependency and impact. Ecologists should tailor survey protocols accordingly:

High-Dependency Sectors (agriculture, forestry, fisheries, water utilities):

- Intensive ecosystem service quantification

- Detailed physical risk scenarios

- Supply chain nature dependency mapping

High-Impact Sectors (mining, construction, manufacturing):

- Comprehensive biodiversity impact assessments

- Restoration effectiveness monitoring

- Regulatory compliance documentation for transition risks

Financial Sectors (banking, insurance, investment):

- Portfolio-level nature risk screening

- Due diligence protocols for nature-exposed assets

- Scenario analysis support for climate-nature interactions

Practical Implementation: Survey Protocols for Ecologists Meeting 2026 Standards

Adapting Field Methodologies

Implementing ISSB Nature Disclosures and BNG: Survey Protocols for Ecologists Meeting 2026 Corporate Reporting Standards requires practical adjustments to field operations:

Phase 1: Pre-Survey Planning

- Conduct stakeholder interviews to identify material nature dependencies

- Review corporate sustainability reports to understand existing disclosure gaps

- Align survey scope with IFRS S1 and S2 reporting boundaries

- Establish data quality standards meeting investor-grade requirements

Phase 2: Field Data Collection

- Use standardized habitat condition assessment forms enhanced with ecosystem service indicators

- Document spatial relationships between operations and nature dependencies

- Photograph and georeference key features supporting materiality claims

- Collect quantitative data suitable for financial risk modeling

Phase 3: Analysis and Reporting

- Calculate traditional BNG metrics alongside nature-related risk indicators

- Prepare dual-purpose reports serving planning authorities and corporate disclosure teams

- Include narrative explanations connecting ecological findings to business implications

- Provide recommendations aligned with nature-positive business strategies

For small development projects, simplified protocols can still incorporate ISSB-relevant data points without disproportionate cost increases.

Technology and Tools for Enhanced Surveys

Modern survey technology facilitates the data richness required for ISSB disclosures:

| Technology | Application | ISSB Benefit |

|---|---|---|

| Mobile GIS apps | Real-time spatial data collection | Precise dependency mapping |

| Remote sensing | Landscape-scale habitat monitoring | Temporal trend analysis |

| Biodiversity metric calculators | Automated unit calculations | Consistent, auditable metrics |

| Ecosystem service models | Quantifying service provision | Financial materiality quantification |

| Blockchain verification | Data integrity assurance | Investor confidence in disclosures |

Investing in these tools positions ecological consultancies to serve the growing market for corporate biodiversity assessments that meet international disclosure standards.

Quality Assurance and Verification

The shift toward investor-grade nature disclosures elevates expectations for data quality and verification:

✅ Competency requirements: Surveyors may need additional training in financial materiality assessment and corporate reporting frameworks

✅ Peer review processes: Complex assessments supporting material disclosures should undergo independent technical review

✅ Audit trails: Comprehensive documentation of methodologies, assumptions, and data sources to support external assurance

✅ Standardization: Adoption of internationally recognized protocols (TNFD, Science Based Targets for Nature) alongside local BNG requirements

✅ Continuous improvement: Regular updates to protocols as ISSB standards evolve through consultation feedback

Guidance for developers should emphasize these quality assurance elements to ensure survey outputs support both planning applications and corporate disclosure obligations.

Preparing for the Exposure Draft and Beyond

Engaging with the Consultation Process

The 120-day consultation period following the October 2026 Exposure Draft represents a critical opportunity for ecological professionals to shape final standards. The ISSB's previous consultation on SASB Standards enhancements received 238 comment letters and 226 survey responses during a 150-day period, demonstrating significant stakeholder engagement.

Ecologists should prepare to contribute technical expertise on:

- Feasibility of proposed metrics: Can recommended indicators be reliably measured through field surveys?

- Cost-benefit considerations: Do disclosure requirements impose proportionate burdens relative to decision-usefulness?

- Methodological guidance needs: Where do surveyors need additional technical specifications?

- Sector-specific challenges: What unique considerations affect nature assessment in different industries?

Professional associations, ecological consultancies, and individual practitioners can submit formal comment letters or participate in stakeholder roundtables. Early engagement ensures that final standards reflect practical realities of ecological fieldwork.

Building Capacity and Expertise

As ISSB Nature Disclosures and BNG: Survey Protocols for Ecologists Meeting 2026 Corporate Reporting Standards converge, professional development becomes essential:

Recommended Training Areas:

- 📚 Corporate sustainability reporting fundamentals (IFRS S1, S2 structure)

- 💼 Financial materiality assessment techniques

- 🌐 TNFD framework and nature-related risk categories

- 📊 Ecosystem service valuation methodologies

- 🔍 Assurance and verification standards for sustainability data

Many ecological professionals excel at species identification and habitat assessment but lack exposure to corporate reporting contexts. Bridging this knowledge gap creates competitive advantages as demand grows for biodiversity assessments that support corporate disclosures.

Market Opportunities and Business Development

The integration of nature disclosures into mainstream corporate reporting creates substantial market opportunities:

Emerging Service Lines:

- Nature dependency and impact assessments for corporate portfolios

- Baseline surveys designed for multi-year disclosure tracking

- Verification services for nature-related corporate claims

- Training and capacity building for corporate sustainability teams

- Integration consulting connecting ecological data to financial reporting systems

Client Expansion:

- Beyond traditional development sector clients to include corporate sustainability departments

- Financial institutions requiring nature risk due diligence

- Investment managers seeking portfolio-level nature metrics

- Supply chain managers assessing upstream nature dependencies

Landowners interested in selling biodiversity units may also benefit from ISSB-aligned assessments that demonstrate corporate-grade nature-positive outcomes, potentially commanding premium prices.

Long-Term Strategic Positioning

Looking beyond 2026, ecological consultancies should position themselves strategically:

Build Partnerships:

- Collaborate with sustainability reporting consultancies lacking ecological expertise

- Establish relationships with corporate sustainability officers in nature-dependent sectors

- Partner with technology providers developing nature disclosure platforms

Invest in Infrastructure:

- Develop proprietary methodologies translating ecological data to financial materiality

- Create template reporting frameworks aligned with ISSB standards

- Build databases of ecosystem service values and nature risk indicators

Thought Leadership:

- Publish case studies demonstrating ISSB-aligned survey approaches

- Present at corporate sustainability conferences, not just ecological forums

- Contribute to standard-setting processes shaping future disclosure requirements

The firms that successfully navigate this transition will find themselves at the intersection of ecology, finance, and corporate strategy—a position offering both professional fulfillment and commercial success.

Conclusion: Bridging Ecology and Finance Through Standardized Disclosure

The convergence of ISSB Nature Disclosures and BNG: Survey Protocols for Ecologists Meeting 2026 Corporate Reporting Standards represents more than a technical update to survey methodologies. It signals a fundamental shift in how society values and accounts for nature. Ecological data, once confined to planning applications and conservation assessments, now directly informs investment decisions and corporate strategy.

For ecologists and biodiversity professionals, this evolution presents both challenges and opportunities. The challenge lies in expanding technical competencies beyond traditional ecological expertise to encompass financial materiality, corporate reporting frameworks, and investor information needs. The opportunity lies in positioning ecological knowledge as essential infrastructure for the sustainable economy—as fundamental to corporate disclosure as financial audits.

Actionable Next Steps for Ecological Professionals

Immediate Actions (Q2-Q3 2026):

- 📖 Review the ISSB Exposure Draft upon release in October 2026

- 🎓 Enroll in training on corporate sustainability reporting and TNFD frameworks

- 🔄 Audit current survey protocols to identify gaps relative to anticipated ISSB requirements

- 🤝 Initiate conversations with corporate sustainability teams in your client base

- 📝 Prepare consultation responses based on field experience and practical constraints

Medium-Term Strategies (Q4 2026-2027):

- 🛠️ Develop enhanced survey templates incorporating nature-related risk indicators

- 💻 Invest in technology supporting spatial analysis and ecosystem service quantification

- 📊 Create case studies demonstrating ISSB-aligned assessments for different sectors

- 🌐 Build partnerships with sustainability reporting consultancies

- 📢 Establish thought leadership through publications and conference presentations

Long-Term Positioning (2027 and beyond):

- 🏢 Expand service offerings to include corporate nature disclosure support

- 🔍 Develop verification and assurance capabilities for nature-related claims

- 🎯 Specialize in high-dependency or high-impact sectors requiring sophisticated nature assessments

- 🌍 Participate in ongoing standard-setting processes as ISSB standards evolve

- 📈 Scale operations to meet growing demand for investor-grade nature data

The October 2026 Exposure Draft will provide concrete technical specifications, but the strategic direction is clear: ecological survey protocols must evolve to serve corporate disclosure needs while maintaining scientific rigor. By proactively aligning methodologies with emerging standards, ecological professionals can ensure their work remains relevant, valuable, and impactful in an economy increasingly recognizing nature as a material financial consideration.

The future of ecological surveying lies not just in measuring biodiversity, but in translating those measurements into the language of business risk, opportunity, and value creation. Those who master this translation will find themselves indispensable partners in the transition to a nature-positive economy.